Receive free Cryptocurrencies updates

We’ll send you a myFT Daily Digest email rounding up the latest Cryptocurrencies news every morning.

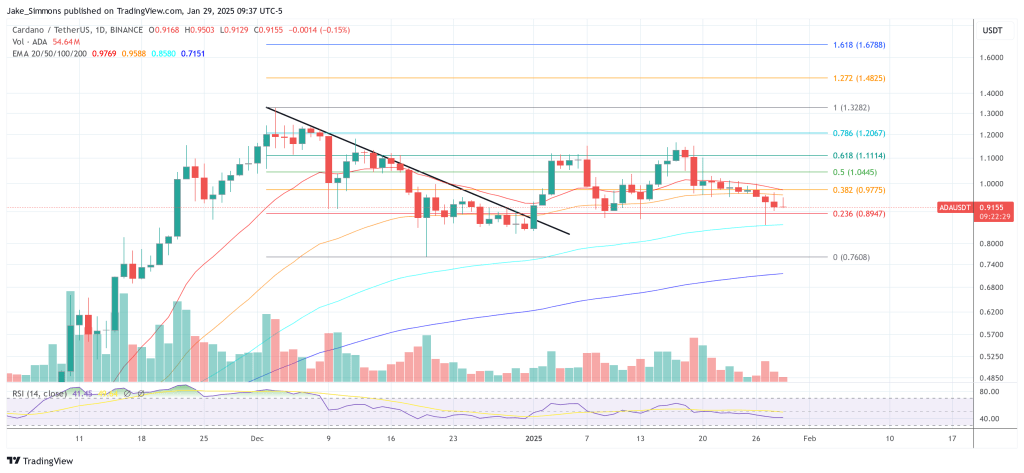

Rapidly rising electricity prices should be bad news for cryptocurrency miners, right? Boutique investment house Kuros Associates believes so, having shorted US-listed Microstrategy and Riot Blockchain in spite of being a short term bitcoin bull.

Miners “have a big problem [with] the rising cost of energy, and that’s not going away any time soon,” said Tancredi Cordero, chief executive at London-based Kuros. “The smart trade would be a put trade expiring in Q3. [Electricity] prices will skyrocket in the summer and that will translate into lower growth margins for these companies.”

What sounds a logical trade may turn out to be a gamble, however, because when it comes to crypto’s costs of production there’s a lot we don’t know.

Bitcoin miners’ average cost of production globally has dropped by almost a fifth in the past fortnight, JPMorgan estimates. Having hovered between $18,000 and $20,000 for most of 2022, the aggregate cost of minting a coin has fallen to about $15,000. And since the start of the year it appears that the least efficient miners have been dropping out of the game.

JPMorgan’s approach is to treat bitcoin like a commodity and apply a marginal cost of mining. The formula used is taken from a 2018 paper authored by Adam Hayes of the Hebrew University of Jerusalem, whose cost assumptions once provided a very approximate lower bound for the market price:

To arrive at an aggregate figure, JPMorgan takes the current market price, hash rate and difficulty then runs them though the Hayes methodology — though the broker concedes that its central input, a $0.05 per kWh cost of electricity, can only ever be a guess. Its benchmark, the Digiconomist Bitcoin Electricity Consumption Index, stopped including an estimate of hardware efficiency in mid 2020,. The analysts now have to back-engineer a number out of Cambridge University’s Cambridge Bitcoin Electricity Consumption Index, which estimates blockchain’s daily electricity load:

Relying on an assumption for one of the key inputs of mining costs is clearly not ideal. However, given it is such an important variable, and the electricity cost of individual miners is often based on bilateral agreements with electricity producers, there is often little incentive for privately held miners to disclose these costs. Arcane Research have estimated that North American publicly listed miners such as Core Scientific, Marathon, Riot, Hut 8 and Bitfarms face electricity costs of between $24 and $40 per MWh, or $0.024 and $0.04 per kWh, based on the most recent public disclosures. While this suggests that our $0.05 per kWh electricity cost assumption may if anything be modestly on the high side for previous years, there can clearly be considerable variability.

The baseload index points to network consumption falling on an annualised basis from 120TWh at the start of June to around 93TWh. Meanwhile, bitcoin’s hash rate has barely budged. That suggests either that miners are retiring their least efficient rigs or that the lower-cost operators have been increasing capacity, JPM concludes:

This bears some echoes of the first half of 2018 as the decline in bitcoin prices to or even modestly below our estimate of production cost was associated with an increase in average efficiency of mining hardware rather than a drop in hash rates, until hash rates eventually declined in end-2018. When the halving of bitcoin block rewards in May 2020 effectively doubled the production cost, miners responded relatively swiftly through a combination of an increase in efficiency of mining hardware and reduction in hash rates, effectively implying that less efficient rigs were taken off-line at the time. The next halving event will likely take place in May 2024, and could see similar dynamics.

It’s also worth emphasising that while mining cost estimates can form the lower bound for bitcoin, what really matters is sentiment:

Publicly listed mining companies account for around 20 per cent of all mining activity, according to JPMorgan. These companies should have buying power, better access to finance and more honed survival instincts and than rivals with artisanal mining fleets — yet the market has not shown much confidence in their ability to move down the cost curve and ride out crypto winter.

Nasdaq-listed Core Scientific, Marathon and Riot have all tumbled nearly 80 per cent in the year to date and many operators have been selling down their reserves, either to fund operating costs or meet debt covenants.

Kuros Associates has been paring back its bet against US bitcoin miners in response to last week’s crypto market bounce, along with recent bouts of heightened volatility across digital assets. Bitcoin could yet double over the summer before tumbling to $1,000 by the end of the year, says Cordero, as institutional investors and hedge funds with crypto-only mandates move out of smaller cap tokens and into the bigger names. “But when implied and realised vol go down on options in this space, we’ll probably reopen the trade.”

You can get bonuses upto $100 FREE BONUS when you:

💰 Install these recommended apps:

💲 SocialGood - 100% Crypto Back on Everyday Shopping

💲 xPortal - The DeFi For The Next Billion

💲 CryptoTab Browser - Lightweight, fast, and ready to mine!

💰 Register on these recommended exchanges:

🟡 Binance🟡 Bitfinex🟡 Bitmart🟡 Bittrex🟡 Bitget

🟡 CoinEx🟡 Crypto.com🟡 Gate.io🟡 Huobi🟡 Kucoin.

Comments